Let’s get things straight. Have startups in the history of time received a term sheet after their very first meeting with a VC? Yes. Have founders raised monumental rounds that were oversubscribed within a week? Of course. Outliers will always exist, and it would be wonderful if everyone fit into this category. But they don’t. The reality is that raising a Series A takes a lot of time — five months on average — from when a company starts building their narrative (story and deck) to the time they see the wire hitting their company bank account. Where does this number come from? We didn’t just make it up. It’s the average time it took for our last twelve portfolio companies to complete their Series A financing, where the lead wasn’t an existing investor and the total round size was $8M USD or more.

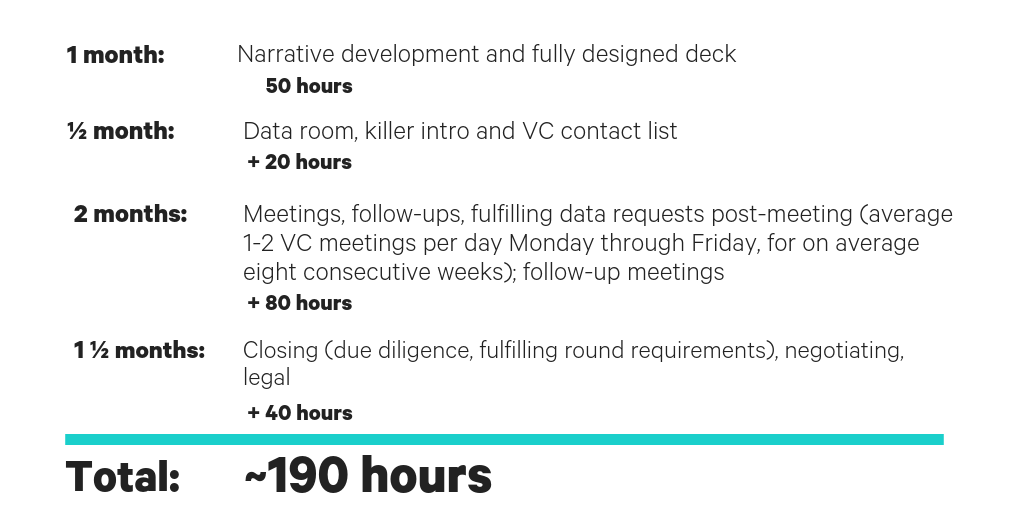

Let me go a step further and break down exactly how these founders spent their five months:

What if you can’t afford to carve out five full months?

Sorry to break it to you — and this is the cold, hard truth — but a lot of other excellent founders will dedicate an enormous amount of time, energy and resources to fundraising within a well-defined and continuous period. And because there are plenty of founders who are 100 percent committed to the process, you will unknowingly be competing for VC dollars with a far better-prepared, organized and driven category of entrepreneur.

In my opinion, on-and-off fundraising simply doesn’t work. If you can’t strap in and give it a five-month go in one shot (assuming your business has the merits to raise and it won’t fall apart in your absence), then you aren’t doing your shareholders, employees and co-founders the justice they deserve. Again, there will always be an example of a bleeding-edge startup with a world-class team building an insane product in a white-hot space that gets term sheets thrown at them left and right. But that’s not what we’re optimizing for. We’re optimizing for the 99 percent of companies that don’t fit into this rare category.

Time to succeed

Friendly reminder: you need enough runway to raise. Miscalculating the amount of time it takes to secure funding is a broken record we refuse to play at Real. From the day their seed rounds close, our CEOs are informed that their number one objective is not to run out of money. It’s easier said than done, we know. So why do we say it that way? The CEO’s job, among many other things, is to make sure the company is capitalized to get from seed to Series A. It’s extremely dangerous when the CEO doesn’t time the validation of the core business assumptions used to get the company from seed to Series A with the net burn rate of the business. Let’s walk through some possible scenarios:

SCENARIO 1: VICTORY IS MINE

- 12+ months runway

- Core business assumptions validated

- Can dedicate five consecutive months to fundraising

- Strong conviction from the board

SCENARIO 2: EYE OF THE TIGER

- 8 months runway

- Core business assumptions validated

- Can dedicate five consecutive months to fundraising

- Strong conviction from the board

SCENARIO 3: DON’T STOP BELIEVING

- 8 months runway

- Have executed half or more of the core business assumptions

- Belief from founders and board in the business

- Need an additional 3–6 months runway to crush assumptions to raise an A

- Raise an internal/external bridge round with 5+ months of runway left

SCENARIO 4: 1,000 PAPER CUTS

- Less than 6 months runway

- Have validated some but not the majority of core business assumptions

- Have not begun any fundraising process

SCENARIO 5: DEATH VALLEY

- Less than 6 months runway

- Have not validated core business assumptions

- Have no active plan for securing bridge or interim financing

Getting to the term sheet

You need to convert 1.5% of your VC intros into a term sheet.

Below is a blended average summary of fundraising pipeline activities from a sample of our portfolio companies that raised a Series A in the last 12 months. Keep in mind that the vast majority of these companies fit in the above scenarios: “Victory is Mine” or “Eye of the Tiger.” Also, take into consideration that the email intros sent to VCs were done through trusted warm introductions. This also statically shows that “Nos” are just part of the game. If you come well-prepared, confident, backed by your team and board, and are persistent, you should come out with a term sheet (or two) in the end.

This is an oversimplified funnel. In reality, between steps I-IV, there are countless follow-up emails, scheduling conflicts and follow-up conversations.

Keep your eye on the prize

You will need to block two consecutive months of your life just for pitching and meetings. To do this, you need to be organized and capable of getting all of your email intros out quickly. In the pipeline averages above, the founders would do the following:

- Set a block of time for VC meetings (i.e from Sept 1st to October 30th). This is not fluid or flexible. Once you commit to this time period, stick with it. If you live outside of the Valley book a Sonder 🙂 or an Airbnb for the full term and call it home. You might fly home for a weekend to take care of the business or personal matters and head back to the Valley before the first meeting on Monday.

- Make sure all email intros are sent within a period of five days or less. Some VCs take longer to respond to emails and you want to book two to three meetings per day (ahead of time) so that you can build enough momentum during your fundraising process.

Build your VC target list wisely

About once a month an entrepreneur asks our team to introduce them to some well-known VC at some top-notch firm. And about once a month we ask that entrepreneur why that VC at that brand name firm is who they should connect with. The answer is never surprising: because they are well known. Before you go bananas and list every Forbes Midas List VC from every reputable firm on a spreadsheet titled ‘VC Intros’, let’s take a minute to think about building your target VC list a bit more strategically. Here is how we break down the criteria:

1. Firm:

- Stage appropriate

- Cheque-size appropriate

- Your industry/market fits with theirs

- Number of new investments/year

- Will they invest in your region? (Not every company is based in Silicon Valley and some investors simply won’t cut checks outside of it ☹)

- No competing investments

2. Partner

- Years of investment experience

- Track record (previous founder, exits, roles, awards, accolades)

- Expertise/areas of strong understanding

- Their portfolio

- Bonus: If you have info on how entrepreneurs rate the quality of working with that partner, even better!

Based on these criteria, you’ll be able to find the ideal VCs to pitch. And once you have your list of ±60 firms to target, you can send your board, investors and advisors a spreadsheet that looks something like this:

How email intros should work

Requesting that your board, investors and advisors introduce you to top VCs in their network is no small ask. While you may feel they are obligated to help you succeed, their VC intros won’t have much impact — or could even hurt their reputation — if the email isn’t compelling, articulate and polished. That’s why it’s your responsibility to draft and nail the killer email intro for them to send on to their VC network.

The double opt-in email

The best way to request an intro is through what we call a double opt-in. In this format, your advisor/board member or investor is personally reaching out to their VC contact and asking them if they would like an introduction. This is the preferred format because:

- It doesn’t put the recipient of the introduction on the spot, and

- It gives the recipient of the introduction an immediate quality filter of the company based on who the referral is from

The killer email intro

Much like the thought and consideration you put into building your narrative, you will need a powerful blurb that highlights the opportunity, your success, team and major insights in a short few paragraphs.

Here’s an example:

Subject Line: Would love to introduce you to Smello-Vision

Hi (investor’s name),

One of the companies I advise, Smello-Vision, has asked me to connect you with them, given your interest and investments in category-defining technologies. The founder and team are world-class and they have done a tremendous amount with very little in funding. Please let me know if you would like an intro — more info below. I’m very bullish on this one!

The above section will ideally be personalized and tailored to each VC

— — — — — — — — — — — — — –

About Smello-Vision

Nine billion people around the world use scent to guide their judgment to make important decisions every day. While the Internet has transformed nearly every industry and facet of life, its application is largely limited to the function of transmitting and receiving bits and bites.

Smello-Vision is a device-agnostic multi-sensory technology that activates neurons by emitting ultra-low-frequency waves to emulate the smell, taste and touch receptors in our bodies. Doing this manifests the digital world into the physical world, unleashing endless possibilities.

Founded in January 2016, we’ve deployed our technology to over 100,000 people in 22 countries. Through our patented Smell Instant technology, we saw an overall increase in user engagement by 75 percent and conversion rates by 88 percent on deployed websites and applications.

In the past few months, we recruited world-renowned PhD, Adamo Pizzaiolo, from the MIITT Lab of Neuroscience to join us as our Chief Scientist. We struck a four-year $5M deal with Pizza Hat to directly integrate our technology into their e-commerce experience and were recently named Wiredz Most Innovative Startup of the Year.

Best,

Jess James

Practice your pitch

As with everything, practice makes perfect. Before getting email intros to your top VC targets, make sure you utilize your board, advisors and local friendlies to get their feedback on your narrative. During these friendly meetings, you will often find ways to better organize your pitch deck or tweak a few slides for stronger impact.

Time management FTW

Here’s what running a tight and organized fundraising process looks like in terms of time management. Notice how all the meetings are lined up two months in advance, with no gaps or off periods between each week.

This is because the founder sent out all of the emails within five days and was able to incentivize the other VCs to meet during the same time period. If you run this process properly, you are sure to build momentum which will create more urgency for VCs to make a decision.

I also don’t recommend taking more than three meetings a day, because by week two or week three you’ll have follow-up meetings, data requests to fulfill and possibly partnership pitches. Plus, you’re only human, so by the third meeting you’ll most likely be tired and mentally drained — not to mention shuttling around the Bay Area can be a nightmare in terms of traffic.

Once you start meeting VCs and finding partners who are interested in your business, you will need to think about how compatible they and their firm would be with your company.

I use the following rubric to advise entrepreneurs on how to evaluate the VCs they could potentially work with. After all, you’re not just getting money from this individual and firm, you’re getting a new business partner. And once the honeymoon period with your new VC wears off, it will become immediately clear whether or not the two of you are aligned across major areas of the business.

Firm Tiers

The idea of classifying firms by tiers is relevant when you take into consideration the value of the firm’s brand alongside the value of the firm’s partner who will lead the deal.

Tier 1 firms

These are your legacy VC firms that have been around for decades and have track records that speak for themselves. There are less than a dozen of these.

Tier 2 firms

We typically classify these as newer firms that have emerged within the last 10–15 years. They have phenomenal partners and have made some interesting and very relevant investments, but their brand notoriety amongst most entrepreneurs is still nascent and they have only raised a handful of funds.

Tier 3 firms

These can be strategics, corporates or super niche investors that have a narrow/limited focus. They can certainly still add tremendous value and bring domain expertise. Their primary reason for investing isn’t driven by a 10X return, but rather to build corporate synergies and knowledge, and in most cases, to obtain access to information and data to stay ahead in their competitive landscape.

Best case scenarios

In a perfect world, you will get a term sheet from a Tier 1 firm with a partner who checks all of the above criteria. But what if you get two term sheets: one from a Tier 1 firm, but a partner who checks less than two of the above boxes, and another from a Tier 2 firm with a partner that checks all of the boxes? Which term sheet do you take? This actually happens more frequently than you’d think, especially if you follow the fundraising process outlined in this post. It becomes an even more difficult decision when the valuations are similar or one is only slightly higher. The whole point of this exercise is to force yourself to think about what really matters when finding the right VC, and hopefully it will help you make the best decision for your company.

But getting to the point of a term sheet means that you’ve not only run a smooth process and got the meetings with the VCs, but that you’ve also gone into those meetings impeccably well prepared.

In the next post, I’ll dig into the optimal way to run your meetings to win. In the meanwhile, remember that preparation can make the difference between multiple terms sheets or at best, one VCs interest. So know when you’re ready to blast the emails and get your meetings lined up. That way, you’ll be able to pitch your laser-focused company narrative to an audience that knows that time is of the essence.

**********

For more insights into the VC fundraising process as well as founder stories, ecosystem deep dives and industry trends, sign up for our newsletter and follow us on Twitter, LinkedIn and Facebook.

April 10, 2019

April 10, 2019  Sam Haffar

Sam Haffar